If you want to start an online book store, the data is…

How to Open a US Bank Account For Non-Residents

If you are a non-resident trying to open a US bank account for your ecommerce business or offline store, you have probably already hit a wall. Most US Bank websites ask for a Social Security Number, which you don’t have at the moment. So you ask yourself, how to open a US bank account for non-residents?

Traditional US banks require clients to visit a physical branch to register. And the banking advice you find online is either outdated, misleading, or written for Merchants who are already living in the US with valid documentation.

This detailed guide cuts through all of that. So, whether you are a merchant, freelancer, an eCommerce store owner, an entrepreneur running a US LLC from abroad, or simply a merchant who needs to receive USD payments without paying high wire fees, this is the complete, step-by-step breakdown of how to open a US bank account as a non-resident from anywhere in the World.

We will cover every route available to you, what documents you actually need, and where the ITIN fits into this journey — because for most non-residents, it is the missing piece nobody talks about.

Table of Contents

Can a Non-Resident Open a US Bank Account?

Yes, you can, but the available options depend heavily on your situation and the nature of your business.

Many merchants assume you need to be a US citizen or permanent resident to open a bank account in the US.

That is not true. In fact, you do need the right type of bank, valid documents, and, in most cases, a US business structure to support your application, such as a registered LLC.

There are two main routes available:

Route 1: Open Traditional US Banks (the likes of Chase, Bank of America, Wells Fargo, Citibank) — these US banks require an in-person branch walk-in but are also accessible to non-US residents with the right documents.

Route 2: Fintech / Online Platforms (Mercury, Wise Payments (formerly Transferwise) — these Online Payment platforms provide non-US residents with virtual US bank accounts; they allow fully remote US bank account opening and access but typically require a registered US LLC or other valid business entity.

We will explain further in detail. But first, let us talk about the one document that unlocks almost everything: the ITIN.

What Is an ITIN — and Why Do Non-Residents Need One?

Before diving into the details of opening a US bank account, you need to understand what an ITIN is and why it is a must-have for non-residents operating in the US financial system.

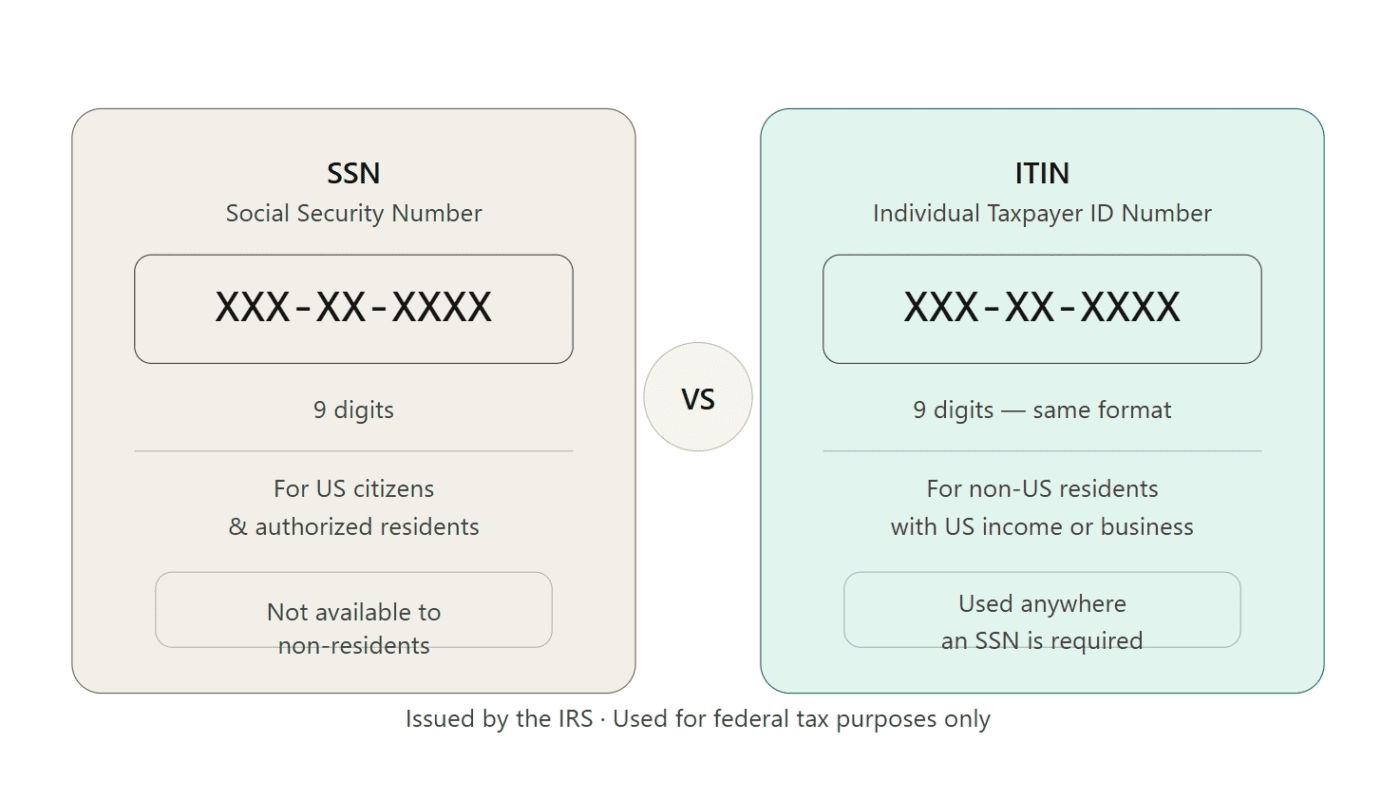

ITIN stands for Individual Taxpayer Identification Number.

It is a 9-digit tax identification number issued by the IRS in the format XXX-XX-XXXX — the same format as a Social Security Number (SSN).

The difference is who it is for: an ITIN is issued specifically to people who are not eligible for an SSN — that is, non-US residents, foreign nationals, and international business owners who have US tax obligations but cannot get a Social Security Number.

In simple terms, wherever the US financial system asks for an SSN, a non-resident uses their ITIN instead.

Where Is an ITIN Required?

This is where most non-resident entrepreneurs get it wrong and get caught off guard. An ITIN is not just used for filing your taxes — it comes up at multiple critical points in your US business formation journey:

1. PayPal Business Account

PayPal requires a personal tax ID, in addition to a business tax ID (EIN), when verifying business accounts.

For non-US residents, that personal tax ID must be an ITIN. Without an ITIN, you cannot fully open, verify, or operate a US PayPal business account.

This is non-negotiable — PayPal asks for it right at the beginning of the verification process while you’re signing up for either a PayPal business or personal account.

2. Stripe Account Verification Stripe payment gateway similarly requires users to have either an ITIN or SSN during identity verification for US-based accounts. Non- US residents without an ITIN will hit a wall at this step.

3. Amazon Seller Account Opening a US Amazon seller account as a non-US resident also requires users’ tax identity verification. Once again, your ITIN is what you provide in place of an SSN when living outside the US.

4. US Tax Filing: If you earn any income connected to the US customers — through your LLC, Ecommerce store, freelance work, or digital products sold to US customers — you may have US tax obligations.

Filing or paying US taxes requires a valid taxpayer ID.

For non-residents, that is your ITIN. You can verify this at the IRS payment portal at payusatax.com, where a tax ID is required to proceed.

5. Certain Bank Account Applications. Some traditional banks and fintech platforms may ask for your ITIN instead of an SSN when opening personal or business accounts.

The bottom line: if you are a non-resident running any US-connected business, your ITIN is not optional — it is foundational.

Step 1: Set Up Your US Business Entity (LLC)

For non-residents, the vast majority of banking options — especially online ones — require a registered US company. Without one, you are limited to personal accounts at traditional banks, which require an in-person visit.

The most popular structure for non-resident entrepreneurs is the LLC (Limited Liability Company). Popular states to register in include:

- Wyoming — low fees, strong privacy protections, no state income tax

- Delaware — preferred if you plan to raise investment or sell the business

- New Mexico — very affordable, minimal annual requirements

Once your LLC is formed, you apply for an EIN (Employer Identification Number) from the IRS. This is your business’s tax ID and is required for every bank, fintech platform, PayPal, Stripe, and Amazon account you open under your business name. Foreign nationals can apply for an EIN online or by fax — no SSN required at this stage.

Step 2: Gather Your Documents

The exact documents required vary by institution, but here is the standard checklist for non-residents:

For Fintech / Online Bank Accounts (Mercury, Relay, Wise):

- Passport (beneficial owner)

- EIN confirmation letter from the IRS

- LLC formation documents (Certificate of Formation/Articles of Organization)

- Proof of business activity (website, invoices, contracts, or client agreements)

- US business address (registered agent address — note: some platforms now require a physical US address, not just a registered agent)

For Traditional Bank Accounts (Bank of America, Wells Fargo, Chase):

- Primary ID: foreign passport or non-immigrant visa with photo

- Secondary ID: foreign driver’s license, debit/credit card, or pay stub

- Proof of foreign home address (utility bill, bank statement)

- Proof of US address (if applicable)

- ITIN or SSN (some banks accept ITIN in place of SSN)

- Initial deposit (ranges from $25 to $3,000+, depending on the bank)

Step 3: Choose the Right Bank

Here is an honest breakdown of your main options in 2026.

Traditional Banks — In-Person Route

Best for: Non-residents who are physically in the US or can travel there.

Most traditional US bank websites are not set up to process applications from people without a Social Security Number, which means an in-person branch visit is almost always required.

Wells Fargo is widely considered the most foreigner-friendly of the major traditional banks — staff is accustomed to working with non-residents who have neither an SSN nor an ITIN. Call ahead, ask to speak with a branch manager, explain your situation (non-US resident, LLC owner, no SSN), and ask for the exact list of documents they need before you visit.

Bank of America does not require an SSN to open a bank account. They require two forms of photo ID plus proof of both a foreign address and a US address. They also offer language services in over 206 languages.

Chase and Citibank are also options, though minimum balance requirements and monthly fees tend to be higher. Call ahead before visiting.

Pro tip: Never walk into a traditional bank as a non-resident without calling first. Ask to email your documents to the branch manager in advance so they can review them before your appointment.

Fintech / Online Platforms — Remote Route

Best for: Non-resident entrepreneurs, eCommerce sellers, freelancers, and remote founders who cannot travel to the US.

Mercury is the most widely recommended fintech banking platform for non-resident US LLC owners. It explicitly serves international founders, requires no US address for the account holder personally (your LLC’s registered agent address works), and offers free ACH transfers, no monthly fees, and clean integrations with Stripe, PayPal, and Shopify.

Note: Mercury has tightened eligibility requirements. Founders from countries on the FATF grey list — including Nigeria and Ukraine — may find their accounts restricted or applications declined. Always verify your country’s eligibility before applying.

What you need: US LLC, EIN, passport, and proof of business activity.

Relay is strong for founders who want to manage cash flow carefully — you can create up to 20 separate checking accounts under one business (useful for separating revenue, taxes, operating expenses, and owner pay). It offers no account fees, no minimum balance, and FDIC insurance up to $250,000 through Thread Bank.

Note: As of 2026, Relay requires a physical US address. A registered agent address alone may not be sufficient — check their current requirements before applying.

What you need: US LLC, EIN, physical US address, passport.

Wise Business Wise is technically an Electronic Money Institution (not a FDIC-insured bank), but it gives you US routing and account numbers for receiving USD payments. Its main advantage is multi-currency capability — you can hold, send, and receive in over 50 currencies at mid-market exchange rates with transparent fees. This makes it ideal for freelancers and founders working across multiple markets.

What you need: Business registration documents, a passport. Does not always require a US entity (check current eligibility for your country).

Lili and Airwallex Both are increasingly recommended alternatives as Mercury and Relay tighten their requirements. Lili is particularly strong for small businesses and offers competitive interest yields on savings. Airwallex offers multi-currency support and is well-suited for eCommerce sellers managing international payments.

Quick Comparison Table

| Platform | Remote? | SSN Required? | ITIN Helps? | FDIC-Insured? | Best For |

|---|---|---|---|---|---|

| Mercury | ✅ Yes | ❌ No | Partially | ✅ Yes | Startups, SaaS |

| Relay | ✅ Yes | ❌ No | Partially | ✅ Yes | Cash flow management |

| Wise | ✅ Yes | ❌ No | No | ❌ No (EMI) | Multi-currency freelancers |

| Bank of America | ❌ In-person | ❌ No (ITIN works) | ✅ Yes | ✅ Yes | US-based non-residents |

| Wells Fargo | ❌ In-person | ❌ No (ITIN works) | ✅ Yes | ✅ Yes | Foreigners in the US |

| Chase | ❌ In-person | Often needed | ✅ Yes | ✅ Yes | Established businesses |

Step 4: Connect PayPal, Stripe, and Other Payment Processors

This is where your ITIN becomes essential again.

Once your bank account is open, you will likely want to connect US payment processors — particularly PayPal and Stripe — to receive payments from US clients and customers.

PayPal will prompt you for a personal tax ID (SSN or ITIN) alongside your business EIN during business account verification. Non-residents must provide an ITIN at this stage. Without it, your PayPal account will remain unverified and limited.

Stripe asks for your SSN or ITIN during identity verification for US-based accounts. The ITIN is accepted in place of an SSN for non-residents.

Amazon Seller Central similarly requires a valid US tax ID for account verification.

This is the step where many non-residents get stuck — they have their LLC and their bank account, but they cannot fully activate PayPal or Stripe because they never got their ITIN. Do not let this be you.

How to Get Your ITIN Fast — and Why The ITIN Is the Best Place to Do It

Getting an ITIN involves filing IRS Form W-7 with your identity documents and proof of foreign status. It sounds straightforward, but it is easy to get wrong — and a rejected application means starting the 8–14 week clock over again from scratch.

That is where TheITIN.com comes in, use this coupon – Dropshippingit to get $50 Off

The ITIN is one of the most trusted ITIN service providers for non-resident entrepreneurs, with a 4.7+ star rating on Trustpilot from over 500 verified clients. They are trained and authorised by the IRS and have helped thousands of international founders — from Latin America, the Middle East, Europe, Africa, and beyond — successfully obtain their ITINs and set up their US business presence.

Here is what TheITIN does:

- Handles all paperwork and filings on your behalf

- Submit your complete application within 48 hours of receiving your documents

- Guides you through the entire process via live chat (including a Spanish-speaking representative, Daniela, for Latin American clients)

- Provides free guidance on opening PayPal, Stripe, and Amazon Seller accounts as part of their support

- Tracks your application and keeps you informed throughout the IRS processing period

What you need to get started: Your US LLC documents, EIN letter, and passport scan. That is it.

How long does it take?

The ITIN submits everything within 48 hours. The IRS then takes 8–14 weeks to process. Nobody can speed up the IRS — but TheITIN ensures your application is submitted the first time correctly, so you are not adding avoidable weeks to the process through errors or missing documents.

What about cost?

The ITIN offers the most competitive pricing for this service on the internet. Comparable services like einexpress.com or itin.com typically charge $400–$500. The ITIN charges significantly less — and currently has a coupon code available that brings the price down even further.

Use this coupon – Dropshippingit to get $50 Off head over to The ITIN Application to Start.

The smart move:

Start your ITIN application at the same time as your LLC formation. The IRS takes weeks regardless, so there is no reason to wait. Every week you delay is a week you cannot fully activate PayPal, Stripe, or file your US taxes.

Apply for your ITIN at TheITIN.com — live chat available, fast response, no hidden fees.

Reasons Non-Residents Get Rejected (and How to Avoid Them)

1. Applying online at a bank that requires in-person visits. Most major bank websites simply cannot process non-resident applications online. If you try to open a Chase or Wells Fargo account on their website without an SSN, you will hit an error. Always call ahead or go in person.

2. Your country is on a sanctions list. The US Department of the Treasury maintains a list of sanctioned countries whose residents cannot open US bank accounts. Mercury and other fintech platforms also have their own restricted country lists. Always confirm eligibility before applying.

3. No US entity. Most fintech banks (Mercury, Relay, Lili) require a registered US LLC or corporation. Applying without one will result in an automatic rejection.

4. Weak business documentation. If your LLC is newly formed and you have no website, no invoices, and no clear business activity, banks may decline on compliance grounds. Have your business website live, and prepare a few invoices or client agreements before applying.

5. Using a registered agent address where a physical address is now required, Relay, in particular, has tightened this requirement. Check what type of US address is currently accepted by your chosen platform before applying.

Tax Obligations: What Non-Residents Need to Know

Having a US bank account and LLC does not automatically create a US tax obligation — but it can, depending on how your business operates. Key points:

- FDIC insurance protects your deposits up to $250,000 per account at US-chartered banks

- Interest income from US bank accounts is taxable and reported to the IRS

- Form W-8BEN may be required by your bank to certify your foreign status and determine whether tax treaty benefits apply

- FATCA (Foreign Account Tax Compliance Act) means your home country bank may be required to report your US financial accounts to tax authorities

- If your LLC generates US-source income, annual tax filing (Form 1120 or 5472, depending on your structure) is typically required

This is why your ITIN matters for tax purposes, too — it is your identifier when filing or paying any US taxes. Consult a US CPA who specialises in international clients to understand your specific obligations.

Alternatives if You Cannot Open a US Bank Account Yet

If you are still working on your LLC or ITIN application, here are stopgap options:

- Wise Personal/Business — receive US bank details and hold USD without a formal US bank account; multi-currency support

- Payoneer — especially useful for marketplace sellers on Amazon, Fiverr, and Upwork; provides US receiving details

- Airwallex — strong for cross-border eCommerce, supports ACH and wire transfers

- International banks with a US presence — HSBC and Citibank sometimes allow non-residents to open international USD accounts from their home country.

These are good temporary solutions, but they are not substitutes for a proper US bank account when it comes to building business credit, integrating with US payroll tools, or meeting platform verification requirements.

Frequently Asked Questions

Can a non-US resident open a US bank account?

Yes. Non-residents can open US bank accounts through traditional banks (with an in-person visit) or fintech platforms (online, with a US LLC and EIN). The right approach depends on your situation and country of residence.

Do I need a Social Security Number to open a US bank account?

No. Many banks and fintech platforms accept an ITIN in place of an SSN. Some fintech platforms (Mercury, Relay, Wise) do not require either SSN or ITIN for business accounts — just an EIN tied to your US entity.

Can I open a US bank account online without visiting the US?

Yes, through fintech platforms like Mercury, Relay, Wise, and Lili — as long as you have a US-registered LLC and EIN.

What is the easiest US bank account to open as a non-resident?

Wise Business is generally the easiest to get approved for. Mercury is the most feature-rich for business founders. For traditional banks, Wells Fargo is the most foreigner-friendly.

Do I need a US LLC to open a US business bank account?

For most fintech platforms, yes. For traditional banks, a US business entity is helpful but not always required if you have an ITIN and can visit in person.

What is an ITIN, and do I really need one?

An ITIN is a 9-digit Individual Taxpayer Identification Number issued by the IRS to non-residents who need a US tax ID but cannot get an SSN. You need it to fully activate PayPal and Stripe, file US taxes, and, in some cases, open a traditional bank account. For any non-resident running a US-connected business, it is essential.

How long does it take to get an ITIN?

The IRS currently takes 8–14 weeks to process ITIN applications. A service like TheITIN.com submits your paperwork within 48 hours, so the clock starts as soon as possible.

Is Wise a real US bank account?

No. Wise is an Electronic Money Institution (EMI), not a US-chartered bank. Your deposits are not FDIC-insured in the traditional sense. It is a useful tool for receiving and converting USD, but for full banking functionality, you will want a proper bank account with Mercury, Relay, or a traditional bank.

Which countries are blocked from opening US bank accounts?

Countries under US Treasury sanctions cannot open US bank accounts. Mercury and other fintech platforms also maintain their own restricted country lists (often tied to the FATF grey list).

Check each platform’s eligibility before applying. The Treasury’s sanctions list is updated periodically at home.treasury.gov.

Conclusion: Your US Banking Roadmap

Here is the complete path from zero to a fully functional US financial setup as a non-resident:

- Form your US LLC (Wyoming, Delaware, or New Mexico are popular choices)

- Get your EIN from the IRS (can be done online as a foreign applicant)

- Apply for your ITIN immediately — don’t wait. The IRS takes 8–14 weeks, and you need it for PayPal, Stripe, Amazon, and US taxes. Use TheITIN.com for the fastest, most reliable application at the best price online.

- Open your fintech bank account (WISE or Relay for most business founders; Wise if you need multi-currency)

- If you need a traditional bank account, call ahead, prepare your documents, and book an appointment at Wells Fargo or Bank of America

- Connect your payment processors — PayPal, Stripe, Amazon Seller — using your EIN and ITIN

The biggest mistake non-residents make is treating the ITIN as an afterthought. By the time they realise they need it to activate PayPal or Stripe, they have to wait another 8–14 weeks. Start it now, run it in parallel with everything else, and your entire US business infrastructure will be ready to go at the same time.

Need help with your ITIN application? TheITIN.com handles everything within 48 hours, offers the most competitive pricing online, and provides free guidance on PayPal, Stripe, and Amazon account setup. Spanish-speaking support is available. Get started at theitin — their live chat team is available now.

Related Posts